Global SSP Fertilizer Market Growth: Trends & Opportunities

- 2026-06-09

Global SSP fertilizer market growth is one of those stories that doesn’t get nearly enough attention — and honestly, that’s surprising given how central single superphosphate remains to smallholder agriculture across three continents. Over the past five years, demand patterns have shifted meaningfully. Crop price cycles, soil health movements, and a broader push to localize fertilizer supply chains are all reshaping the competitive landscape. The conversations happening in procurement offices in Lagos, Nairobi, and Dhaka today look very different from what I was seeing a decade ago.

What’s Actually Driving Global SSP Fertilizer Market Growth

A few interlocking forces are at work. First, phosphorus remains irreplaceable. There’s no synthetic workaround for what phosphate fertilizers do at the soil-plant interface — and that fundamental reality anchors SSP fertilizer demand regardless of commodity price swings.

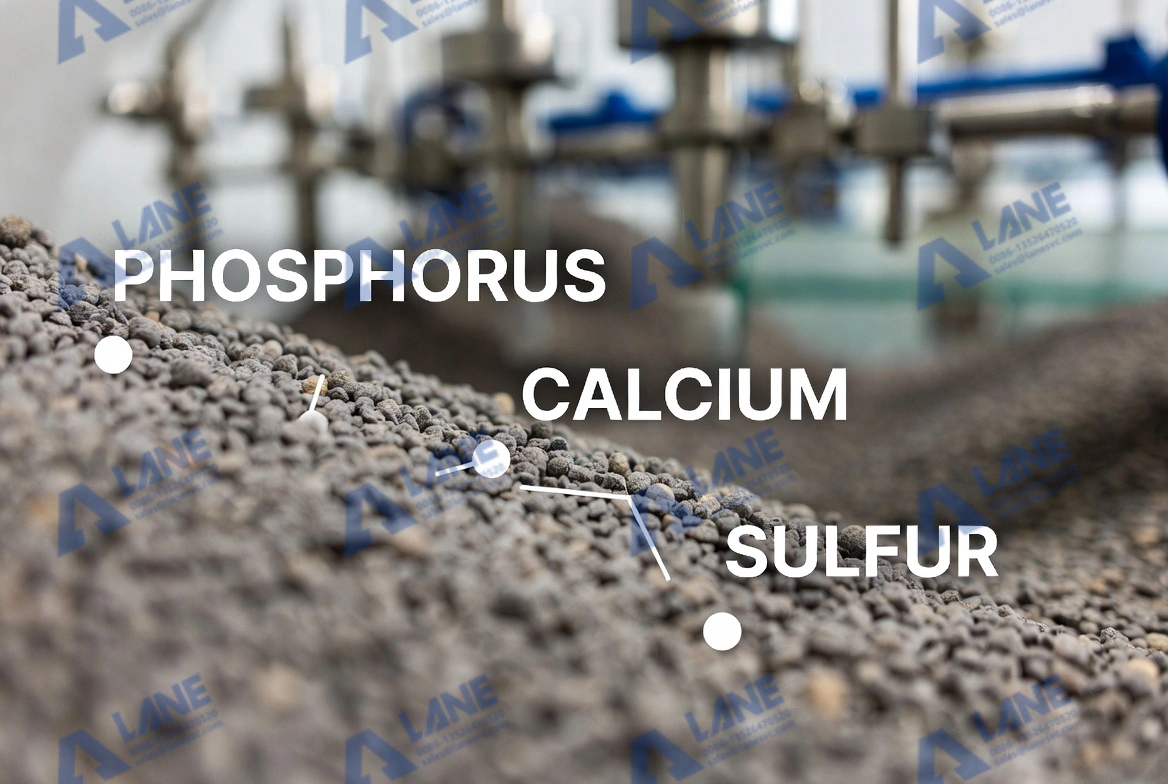

Second, the intermediate-cost positioning of SSP has become a genuine competitive advantage. DAP and MAP carry higher nutrient concentrations, but their price points are brutal for resource-constrained smallholders. SSP, with its 18–20% P₂O₅ content plus sulfur co-benefit, threads a needle that premium products cannot. African markets in particular have responded strongly to this value proposition. In my experience, SSP fertilizer demand in price-sensitive regions consistently holds firmer than analysts expect during commodity downturns.

Third — the localization wave. The supply chain shocks from 2021–2022 changed risk appetites permanently. Regional governments that previously relied on import dependence are now actively supporting domestic production infrastructure. That creates real entry points for new capacity and directly fuels global SSP fertilizer market growth in regions that were once purely import-dependent.

The Regional Picture

Sub-Saharan Africa is where global SSP fertilizer market growth is probably most visible right now. Nigeria, Ethiopia, Kenya, and Tanzania have all seen new plants announced or existing facilities expanding. SSP fertilizer demand in these markets is underpinned by widespread sulfur deficiency in tropical soils, rising crop intensification, and policy tailwinds from programs like the African Fertilizer and Soil Health Action Plan.

Southeast Asia tells a somewhat different story — more fragmented, more competitive with imported product. Vietnam and Bangladesh stand out, though. Vietnam’s export-oriented horticulture sector has pulled consumption upward, while Bangladesh’s domestic rice production programs continue generating baseline phosphate needs that SSP fills efficiently.

South Asia remains the largest absolute consumption zone. India’s SSP sector has matured considerably, with production increasingly consolidated around larger, more efficient plants. From what I’ve seen in the field, the Indian market rewards operational efficiency above almost everything else.

Core Equipment in a Commercial SSP Production Line

You can’t talk about global SSP fertilizer market growth seriously without talking about plant capacity. New SSP fertilizer demand has to be met by new or upgraded production lines. The essential equipment in a commercial SSP facility includes:

- Acidulation reactor— where sulfuric acid meets phosphate rock; residence time and mixing intensity determine product quality at the foundation

- Rotary drum granulator— converts cured SSP mass into consistent granular form for handling and field application

- Rotary drum dryer— removes excess moisture post-granulation to achieve target moisture specifications

- Rotary drum cooler— brings product temperature down to safe packaging conditions

- Vibrating screen— classifies granules to on-spec size, recycling oversize and undersize fractions

- Raymond mill— grinds phosphate rock to the fine particle size necessary for effective acid reaction

- Belt conveyor system— moves material between process stages; critical to operational continuity

- Automatic packaging machine— final step before dispatch, increasingly automated in modern facilities

- Coating machine— reduces caking and improves shelf life in high-humidity storage environments

Manufacturers like LANE have been supplying integrated SSP production lines across Africa and Southeast Asia. What I’ve noticed in recent project reviews is that buyers increasingly evaluate complete turnkey capability rather than sourcing equipment piecemeal — the total-cost-of-ownership calculation has shifted decisively.

Challenges the Market Still Has to Work Through

Let me be honest about the friction points. Phosphate rock quality variation is probably the single biggest headache for SSP producers in emerging markets. When feedstock is inconsistent, process parameters need constant adjustment — and that creates yield variance that downstream distributors hate.

Sulfuric acid availability is another structural issue. SSP is inherently coupled to sulfuric acid supply chains, which means producers in landlocked regions often face logistics costs that erode competitive position versus imported alternatives.

Environmental compliance requirements are also tightening. Fluorine emissions management at the acidulation stage is getting more regulatory attention, particularly in markets where industrial zone regulations are maturing. Plants that invested early in proper scrubbing systems now sit in a stronger competitive position.

Investment Outlook

Global SSP fertilizer market growth projections through 2030 generally land in the 3–5% CAGR range. That’s not spectacular, but it’s steady and real. More importantly, the geographic redistribution of capacity is happening faster than aggregate numbers suggest. Greenfield investment in Africa has attracted serious development finance attention — which tells you where the smart money sees SSP fertilizer demand headed over the medium term. The signals around localization policy, soil health awareness, and price-competitiveness all point in the same direction.

Conclusion

SSP’s position in the global fertilizer mix is more durable than its sometimes-overlooked reputation suggests. Accessible price points, sulfur co-nutrition, and localization suitability keep global SSP fertilizer market growth on a steady upward track even as higher-analysis products compete aggressively for share. The underlying SSP fertilizer demand fundamentals — food security pressure, soil health priorities, cost sensitivity — aren’t going away. Africa and parts of Southeast Asia represent the most dynamic demand environments for the next decade, and the equipment infrastructure, financing models, and policy support are increasingly aligned to serve them.

If you’re evaluating an SSP production project or looking to expand existing capacity, this is the moment to move. Contact LANE for a technical consultation on SSP production line configuration tailored to your feedstock and target market.

FAQ

Q1: What is driving global SSP fertilizer market growth in the near term?

The primary drivers are expanding food demand in Sub-Saharan Africa and South Asia, government fertilizer localization programs, and SSP’s cost advantage over higher-analysis phosphate fertilizers. The sulfur content of SSP also addresses widespread deficiency in tropical soils.

Q2: How does SSP fertilizer demand compare to DAP and MAP in emerging markets?

SSP fertilizer demand holds firmer in price-sensitive markets because SSP offers the lowest per-unit cost for phosphorus delivery. DAP and MAP carry more concentrated nutrient loads but at substantially higher purchase prices — which many smallholder-dominated markets cannot absorb.

Q3: What phosphate rock quality specifications matter most for SSP production?

P₂O₅ content of the rock (ideally above 28%), particle fineness after grinding, and contaminant levels — particularly MgO — are the critical parameters. High magnesia content causes acidulation problems that are difficult to manage operationally.

Q4: How large is a typical commercial SSP production facility?

Commercial SSP plants range from around 50,000 tonnes per year for smaller regional facilities up to 500,000+ tonnes for large integrated complexes. Most new greenfield projects in Africa target 100,000–200,000 tonne/year capacity.

Q5: What environmental controls are required in an SSP plant?

Fluorine gas emissions control at the acidulation stage is the primary concern, typically requiring wet scrubbing systems. Dust suppression at granulation, screening, and packaging stages is also standard practice in modern facilities.

Q6: What is the typical ROI timeline for an SSP production project?

Most feasibility models for African and Southeast Asian projects show payback periods in the 4–7 year range at reasonable capacity utilization. Projects co-located near sulfuric acid sources and port infrastructure for rock imports tend to perform at the better end of that range.

For more details, please feel free to contact us.

Henan Lane Heavy Industry Machinery Technology Co., Ltd.

Email: sales@lanesvc.com

Contact number: +86 13526470520

Whatsapp: +86 13526470520